Investor News

ECT Advance Industry Engagement Initiatives

Environmental Clean Technologies Limited (ASX: ECT) (ECT or Company) is pleased to provide the following update in relation to industry engagement and development.

Highlights:

- ECT becomes advisory committee member of Gippsland Region Hydrogen Cluster (GRHC)

- Hydrogen industry development receiving broad, technology-neutral, bipartisan support

- ‘Green’ hydrogen being championed by a range of stakeholders, but faces significant technoeconomic challenges to become a viable export producer

- ‘Blue’ hydrogen, produced using lignite coupled with carbon capture and storage (CCS), is scalable and affordable, and able to bridge the gap between todays use of lignite and tomorrows zero-emission future

- ECT’s Coldry and COHGen technologies positioned to support the commercial development of a Victorian blue hydrogen industry, with the advantage of lower primary CO2 emissions than conventional coal-based routes, reducing reliance on post-production CCS

- ECT becomes member of the Heavy Industry Low-carbon Transition Cooperative Research Centre (HILT-CRC) in addition to the Future Energy Exports Cooperative Research Centre (FEnEx-CRC)

Gippsland Regional Hydrogen Cluster

The Company recently accepted an invitation to join the Gippsland Regional Hydrogen Cluster (GRHC) as a member of the advisory committee.

The GRHC was formed by the Committee for Gippsland and National Energy Resources Australia (NERA) with the stated purpose to ‘build a competitive clean hydrogen industry in Gippsland that will create jobs, secure investment, generate export income and help lower emissions’.

ECT Executive Chairman, Glenn Fozard previously noted the Company has received a great deal of interest from the investment market and shareholders about the progress of its highly prospective COHgen lignite-to-hydrogen production technology and is currently developing a strategy and associated budget for progression to the next stage of commercialisation.

COHGen leverages the Company’s Coldry and HydroMOR processes to deliver a unique method for producing hydrogen from lignite.

Key benefits of the COHgen process include:

- Up to 70% lower CO2 emissions than conventional lignite gasification-based hydrogen production

- Lower carbon capture and storage (CCS) reliance and cost, due to lower CO2 emissions

- Higher hydrogen yield per tonne of lignite than conventional lignite gasification

- Lower estimated cost than conventional lignite, renewable and natural gas-based hydrogen production routes

- Utilises an abundant, affordable, environmentally friendly catalyst that can be used multiple times.

The broad, bipartisan support from state and federal governments to develop Australia’s domestic and export hydrogen capability has been gaining momentum with a range of initiatives intended to position Australia as a future leader in hydrogen exports.

A technology-neutral approach has been adopted, seeking to harness and develop Australia’s resources to deliver hydrogen production at a cost of less than $2 per kg by 2030.

Hydrogen is produced via two mature pathways:

- Thermochemical: Uses a fossil fuel feedstock to produce hydrogen. This process must be paired with carbon capture and storage (CCS) to produce low or zero-emission hydrogen, also called ‘blue’ hydrogen. Mature technologies include steam methane reforming (SMR), which relies on natural gas as an input, and coal gasification.

- Electrochemical: Involves the use of an electrical current to split water into hydrogen and oxygen. Requires the use of low or zero emissions electricity to produce low or zero-emission hydrogen, also called ‘green’ hydrogen. Mature technologies include polymer electrolyte membrane (PEM) and alkaline electrolysis (AE).

The CSIRO, in its 2019 National Hydrogen Roadmap report, highlighted the pathways to an economically sustainable hydrogen industry in Australia, noting a range of barriers to market activation, including lack of supporting infrastructure and the cost of hydrogen supply, in an effort to focus government, academia and industry on key challenges.

In relation to the cost of hydrogen supply, the report further noted that while hydrogen production from gas and coal (including black and brown coal) are the cheapest, black coal is concentrated in NSW and Queensland, where there are either no well-characterised or only onshore CO2 storage reservoirs that carry a higher social licence risk.

The report states:

Hydrogen production via brown coal in Victoria’s Latrobe Valley, therefore, represents the most likely thermochemical hydrogen production project. A prospective plant would have the advantage of an extensive brown coal reserve sitting alongside a well-characterised CO2 storage reservoir in the Gippsland Basin.

Pending successful demonstration in 2020/2021 and subsequent improvements in efficiencies, hydrogen could be produced in the region for approximately $2.14 -2.74/kg once the commercial-scale production and CCS plant come online in the 2030s.

For Victoria, and particularly the Latrobe Valley, this focus could allow the current CO2-intensive power generation sector to pivot away from burning lignite for electricity production, toward cost-effective, scalable, low and zero-emission hydrogen production supplying domestic and international markets.

ECT’s COHgen technology is targeted at delivering a lower cost lignite-to-hydrogen solution via unique catalyst and process efficiencies. In addition, COHgen sequesters up to 70% of the carbon in solid form, in situ, reducing the need and cost of downstream carbon capture and storage (CCS) plant, and creating valuable carbon by-products.

In addition to COHgen, ECT is positioned to support the transition of Victoria’s world-class lignite resource to low and zero-emission applications such as hydrogen production through two other unique technologies.

- Coldry: anyone wanting to utilise lignite needs to dry it first. Coldry is the gateway drying solution to low and zero-emission lignite applications, including hydrogen.

- HydroMOR: primary iron production. Lignite-based and hydrogen-driven, HydroMOR entails the insitu production of hydrogen from lignite within the process, delivering a low-temperature direct reduction solution with 30% less CO2 than a conventional blast furnace, and at a lower estimated cost.

The ‘green’ hydrogen challenge

Renewable hydrogen is seen by many as the ideal solution, using CO2-free wind and solar to generate the electricity to split water to make hydrogen.

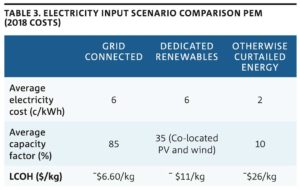

Unfortunately, this approach is higher cost, as outlined in Table 3 of the National Hydrogen Roadmap (right).

Hydrogen Certification

Australia’s Hydrogen Roadmap includes plans for low and zero-emission certification.

Low emission certification is given to hydrogen made with 60% less CO2 than the conventional natural gas-based method.

Zero-emission, or green certification, is given to hydrogen made using 100% renewable generated electricity. Renewable hydrogen advocates place specific emphasis on wind and solar, but hydro, geothermal, tidal and biomass electricity generation may also be used.

At present, based on Australia’s National Energy Market (NEM) generation profile, the grid-connected scenario has a CO2 footprint of ~37kg of CO2 per kg of hydrogen, compared to conventional natural gas-based production of hydrogen which emits ~9.3kg of CO2 per kg of hydrogen, making grid-connected hydrogen production unsuitable for low-emission certification and therefore unsuitable for hydrogen export markets.

The dedicated renewables scenario has zero CO2 emissions, but at much higher cost due to the intermittent nature of wind and solar limiting the hydrolyzers output to 35% of its maximum capacity, pricing it out of reach of the $2/kg target required to compete on export markets.

Using otherwise curtailed wind and solar is more expensive again.

Whilst it is expected that these costs will come down over coming decades, the two biggest price sensitivity factors identified by CSIRO are capacity factor and the price of electricity, followed by capital cost and plant size. This is important to understand because it takes ~50kWh of electricity to produce each kilogram of hydrogen. And even assuming a low wind-solar electricity price of 4c per kWh, the electricity cost alone amounts to $2.00/kg of hydrogen, not including capital cost of the plant and other operational costs.

The CSIRO report shows the current capital and operation cost of the electrochemical pathway needs to fall by at least 75%, while capacity factor needs to increase from 35% to 95% to reach a price range of $2.29-$2.79 per kg, to be comparable with the $2.14-$2.74 price range of lignite-based CCS hydrogen production estimated today.

Lignite-to-hydrogen technology, coupled with CCS, is already within striking distance of the $2/kg price target needed to compete in export markets.

ECT believes its COHgen technology, through further hydrogen production cost reduction, is positioned to bridge the gap between today's use of lignite and tomorrows low and zero-emission future.

ECT BECOMES HILT-CRC PARTNER

Heavy Industry Low-carbon Transition Cooperative Research Centre

The Company is pleased to join the HILT-CRC as an affiliate partner, alongside the likes of Rio Tinto, Glencore and engineering firm, HATCH.

HILT-CRC is positioned to be Australia’s leading collaboration transforming heavy industry for the low-carbon economy. Participants will seek to develop and demonstrate the technologies needed to grow Australia’s economy, unlocking potential value of $48.7 billion in annual revenue and $92 billion in investments, while mitigating CO2 emissions.

Why HILT?

HILT recognises that while heavy industry in Australia has begun to reduce its greenhouse gas emissions, these emissions are particularly hard to abate. Unlike the electricity and transport sectors, heavy industry cannot use off-the-shelf technologies to tap into renewable energies like solar power and hydrogen fuel.

HILT understands that new, carbon-neutral technologies are needed to convert Australian ores to high-value, low-carbon products at globally competitive prices. And they are needed at scale.

Further, HILT acknowledges that Australia has outstanding natural endowments of mineral and clean energy resources. And the global transition to a low-carbon transition represents both opportunities and challenges.

Our Focus

CRCs link companies with researchers to tackle the big challenges. Under HILT, technology developers like ECT will be connected with end-users and other industries along the supply chain, conducting projects that advance low and zero-emission solutions for heavy industry.

Consisting of 3 programs, HILT aims to drive down the emissions intensity of the steel, aluminium and cement industries.

ECT has unlocked the chemistry of lignite, enabling the shift from CO2-intensive lignite-fired power generation to the future low and zero-net emission use of lignite, including:

- Iron and steel production via our HydroMOR process

- Hydrogen production via our COHgen process

- Lignite to diesel production via our CDP-WTE process

Enabled by the Company’s zero-emission lignite drying process Coldry, the Company will seek to develop its suite of solutions for Victoria’s lignite resource.

Future Energy Exports Cooperative Research Centre (FEnEx-CRC)

In addition to the Company’s inclusion under the HILT-CRC, we are also a partner under the FEnEx-CRC.

The FEnEx CRC aims to execute cutting-edge, industry-led research, education and training to help sustain Australia’s position as a leading LNG exporter, and enable it to become the leading global hydrogen exporter, with a focus to help drive hydrogen research efforts to achieve a cost of production under $2 per kilogram by 2030.

Our Focus

There are four research programs:

- Efficient LNG Value Chains

- Hydrogen Export and Value Chains

- Digital Technologies and Interoperability

- Market and Sector Development

ECT is participating under Program 2, Hydrogen Export and Value Chains, which is focused on addressing the following research challenges:

- Processing and delivery methods for cost-effective large-scale hydrogen export

- Target export markets, including key applications and requirements

- Supply chain architecture, design and operations

- Export-class systems and technologies for hydrogen production, storage and delivery

There are two ways the Company seeks to support the thermochemical hydrogen production route, specifically for lignite resources:

- COHgen, which stands for ‘Catalytic Organic Hydrogen generation’, is a novel, low temperature, low emissions hydrogen production technology under development that may provide a lower-cost alternative route to produce hydrogen from lignite

- Coldry, the gateway enabler for lignite-to-hydrogen production, providing the frontend drying solution to COHgen and supporting project developers electing to use conventional hydrogen production technologies (gasification & steam reforming), coupled with CCS

The FEnEx program will assist ECT to validate the scale-up of COHgen in collaboration with industry leaders (energy producers) and end-users (energy consumers) and to identify the range of performance indicators and benchmarks for the production of hydrogen from lignite.

ECT Chairman, Glenn Fozard commented:

“Our increasing involvement across hydrogen industry groups has us well placed to benefit from Government funding, partner collaboration and project roll-out. Our longer-term vision is to build Coldry at large scale in and around the existing Victorian lignite resources and continue to develop COHgen to produce hydrogen from those same commercial Coldry plants.”

The Company looks forward to providing further updates on its innovative hydrogen initiatives as opportunities evolve.

This announcement is authorised for release to the ASX by Adam Giles, Company Secretary.

/// END ///

For further information, please contact:

INVESTORS

Glenn Fozard

Chairman

[email protected] / +61398496203

MEDIA

Adam Giles

Company Secretary

[email protected] / +61398496203