Investor News

'Green' steel plan gives environmentalists false hope

An article ($) by Aaron Patrick in today's Financial Review asks the question:

Should the government spend $500 million building a steel mill to promote technology so space-age it may never be deployed?

The article responds to a recent report by The Grattan Institute titled 'Start with steel: A practical plan to support carbon workers and cut emissions.'

Patrick notes the admirable aim of the report to:

"...help solve one of the great economic, environmental and political challenges of our time: how to phase out Australian coal without turning some 50,000 working men and women, and their families, into climate change carrion."

The Grattan report proposes, among other things, that the taxpayer stump up $500 million to underwrite a $1.5 billion natural gas-fired steel mill that would switch to using 'green' hydrogen in 5 years or so.

All that's then needed is another $200 billion of private investment to build factories in NSW and QLD, and we'll have our very own 'green' steel industry, employing many of the former coal workers and exporting 47.5 million tonnes of 'green' iron and 40 million tonnes of 'green' steel.

But Patrick is critical of the Grattan claim of 'credible economics', noting:

Even steelmakers, which would love more government support as they struggle to reduce carbon emissions, aren't convinced that millions of tonnes of Queensland steel will one day replace coal on ships for Shanghai.

Hydrogen-produced steel "could be decades away", making coal necessary for the foreseeable future, says Mark Cain, the chief executive of the Australian Steel Institute, the industry's lobby group.

"There needs to be a technological breakthrough."

Our own understanding of the economics of hydrogen production set off alarm bells.

A careful examination of the data in the Grattan report exposes several problematic assumptions:

- Buyers must be willing to pay 60% more for 'green' steel

- Renewable hydrogen must drop in price from US$7.70kg to US$3kg to limit the 'green' steel price premium to 60%

- The cost of producing electricity from wind and solar must drop to almost zero in order to produce renewable hydrogen at US$3kg in order to produce 'green' steel at 60% more cost

There's no indication how the cost of renewable hydrogen will be reduced from US$7.70kg to below the US$3kg needed to make 'green' steel economics remotely credible.

The sole goal is to reduce CO2 emissions from iron and steel making. However, the report confirms that even at an ambitiously low renewable hydrogen price of US$2kg, 'green' steel costs 40% more, equating to an abatement cost of US$150 per tonne of CO2 avoided.

Since carbon credits are available for around A$16.00, sticking with coal—and natural-gas-based iron and steel making and offsetting emissions through tree planting is more cost-effective than the proposed 'green' steel plan.

Before we discuss the details, it's important to understand a little about 'green' steel.

'Green' steel is made by stripping the oxygen out of iron ore using renewable hydrogen rather than coal. The byproduct is water rather than carbon dioxide.

In the Grattan proposal, the steel is 'green' because the hydrogen is made by electrolysing water (splitting H2O into H2 and O) using electricity generated by wind and solar. This is called 'green' or renewable hydrogen.

The cheapest and dominant route for industrial-scale hydrogen production is steam reforming, which 'cracks' natural gas to produce hydrogen and CO2.

Electrolysis produces no CO2 but is more expensive.

So far, the technical differences are straightforward.

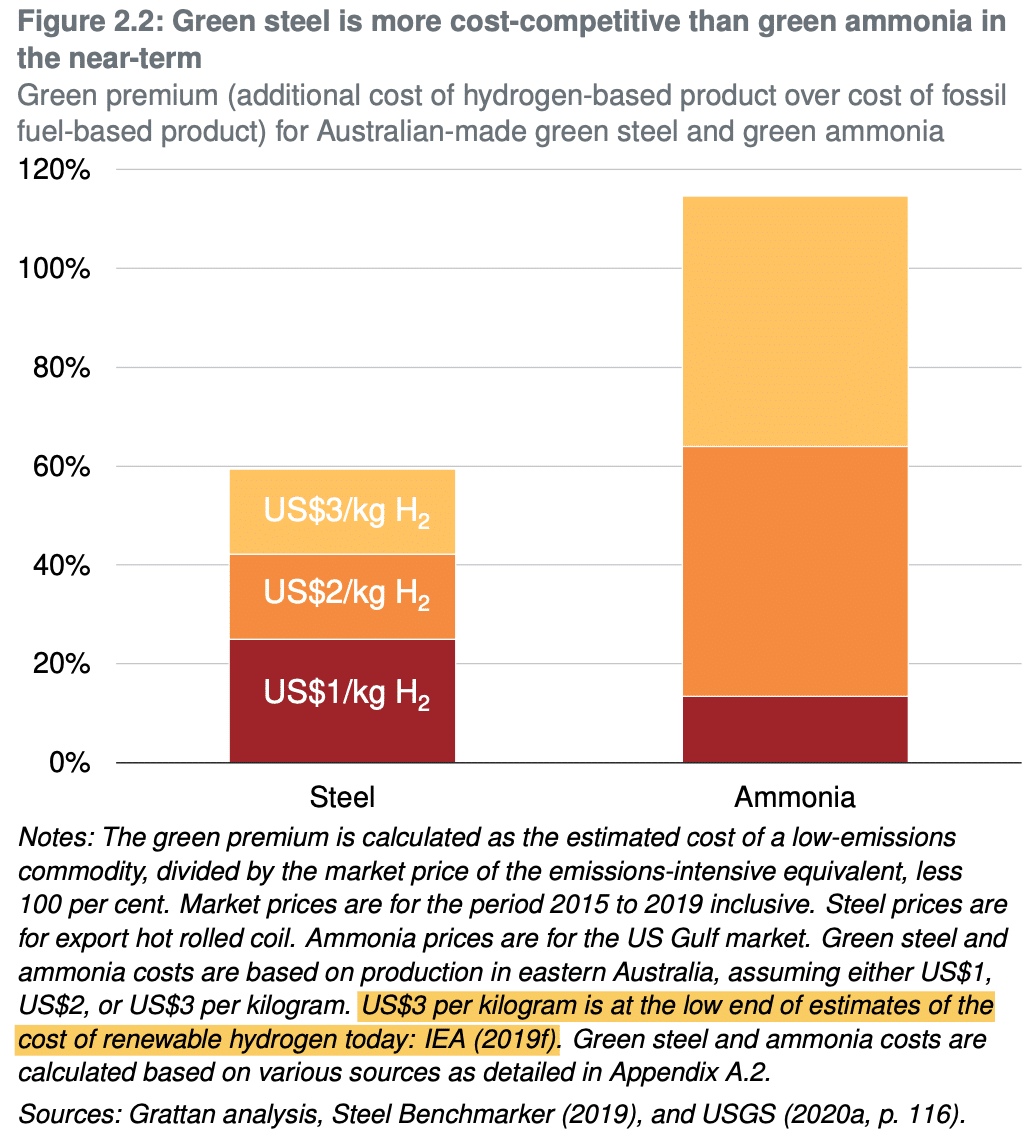

However, when you reach page 20 of the Grattan report, you start to find out just how uneconomic it is to make 'green' steel.

"Hydrogen prices of US$3 per kilogram, which is at the low-range of today’s cost of renewable hydrogen, give a green premium of about 60 per cent for steel..."

Start with steel: A practical plan to support carbon workers and cut emissions

Wood, T., Dundas, G., and Ha, J. (2020). Start with steel. Grattan Institute.

For context, the market price for hydrogen in 2030 is expected to be around $A2.00 to A$2.50kg (US$1.40 to US$1.75), meaning that regardless of how the hydrogen is made, 'green' steel is destined to cost around 40% to 50% more than steel made using coal.

Assuming better than the best

The Grattan report takes the best-case renewable hydrogen cost from the IEA and uses it as its worst-case scenario in a chart on page 21:

Here's a chart from the IEA, the source of the US$3kg reference:

Source: IEA (2019), The Future of Hydrogen, IEA, Paris https://www.iea.org/reports/the-future-of-hydrogen

On that same IEA webpage, you'll also note that hydrogen made from coal or natural gas, with carbon capture and storage, ranges between US$1.50kg and US$2.38kg.

Source: IEA (2019), The Future of Hydrogen, IEA, Paris https://www.iea.org/reports/the-future-of-hydrogen

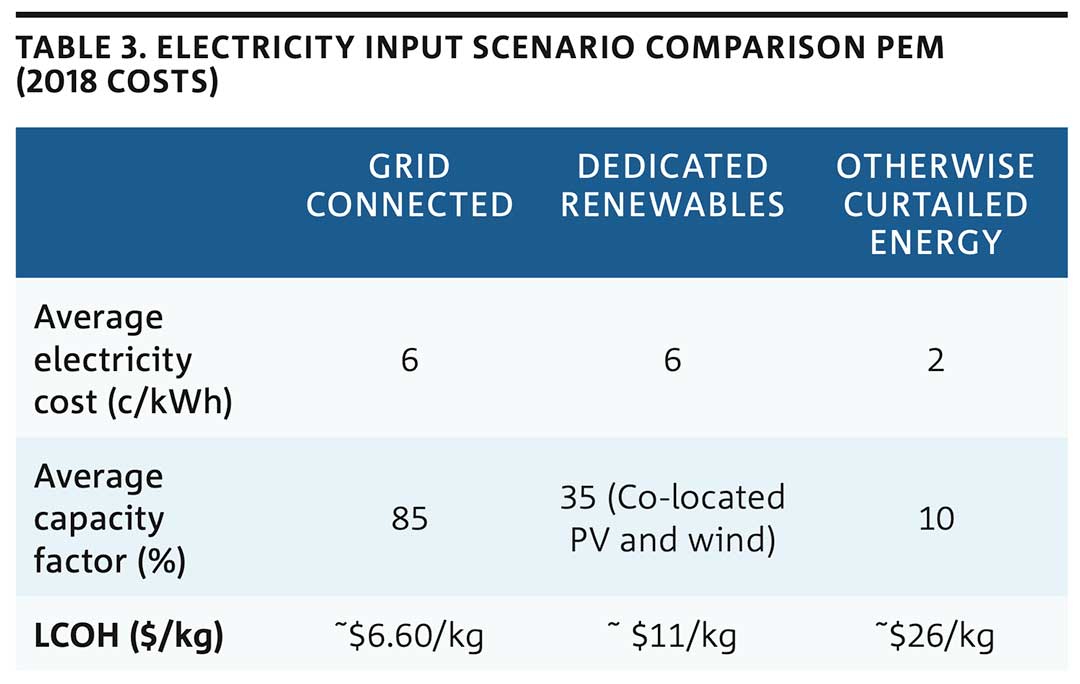

And closer to home, here's the data from the CSIRO's recent National Hydrogen Roadmap, which shows the cost of 'green' hydrogen from dedicated renewables at around ~A$11kg (~US$7.70kg), which sits within the high-end of the IEA range.

Source: Bruce S, Temminghoff M, Hayward J, Schmidt E, Munnings C, Palfreyman D, Hartley P (2018) National Hydrogen Roadmap. CSIRO, Australia.

The Grattan report does not cite a basis for the US$1kg and US$2kg price assumptions and does not say if, when or how renewable hydrogen may achieve these cost points. Unless we've missed something buried elsewhere in the report, they appear to be unfounded.

But you may think it's perfectly reasonable to assume that the cost of renewable hydrogen will come down, even if we don't know exactly how right now. After all, that's what innovation is about. We agree, to an extent, but we need to get at least a ballpark idea of what that cost reduction needs to look like.

How do we work out what needs to happen to actually bring down the cost of electrolytic hydrogen to US$3kg or less?

Luckily, the National Hydrogen Roadmap, on page 19, outlines what's required to bring down the cost of hydrogen in the grid-connected scenario.

Note: Grid-connected hydrogen, as distinct from renewable hydrogen, is simply hydrogen made using electricity provided by the grid rather than dedicated wind and solar power.

Around 83% of electricity generated via the grid comes from coal, natural gas and oil products.

As such, hydrogen made from grid-connected electricity would not be considered compliant with 'green' steel certification.

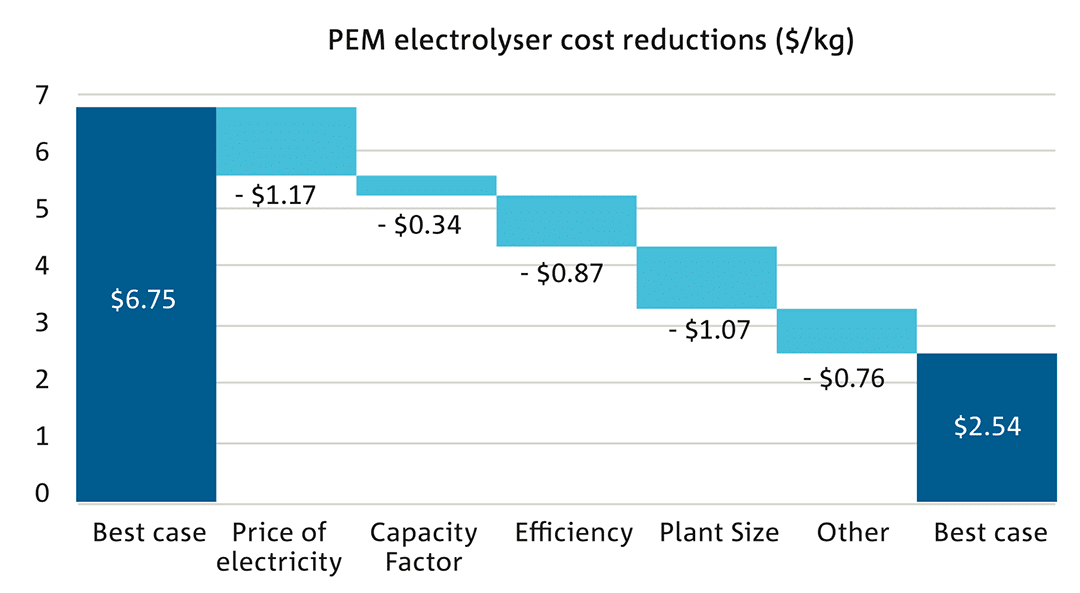

By examining the following projected cost reduction chart for grid-connected hydrogen, we can understand the tremendous challenge 'green' steel advocates face in bringing down the cost of the more expensive dedicated renewable hydrogen production.

The chart below takes the current best-case grid-connected hydrogen cost scenario and breaks down the required cost reduction across various influencing factors to arrive at a future best-case scenario.

Source: Bruce S, Temminghoff M, Hayward J, Schmidt E, Munnings C, Palfreyman D, Hartley P (2018) National Hydrogen Roadmap. CSIRO, Australia.

Let's assume that improvements in capacity factor, efficiency, plant size and other factors can be delivered as stated.

This leaves the largest single component, electricity cost, which must drop by A$1.17/kg to make grid-connected electrolytic hydrogen affordable and competitive with coal—and natural-gas-based methods.

Is this required electricity cost reduction feasible?

We need two pieces of information to find out:

- Electricity required to make 1kg of hydrogen: 50kWh;

- the grid-connected electricity price for the current best-case scenario on the left of the chart: A6c/kWh (taken from Table 3, further up this page)

Calculation: 50kWh x A6c = A$3 of electricity per kg of hydrogen as the starting point under the best-case grid-connected scenario.

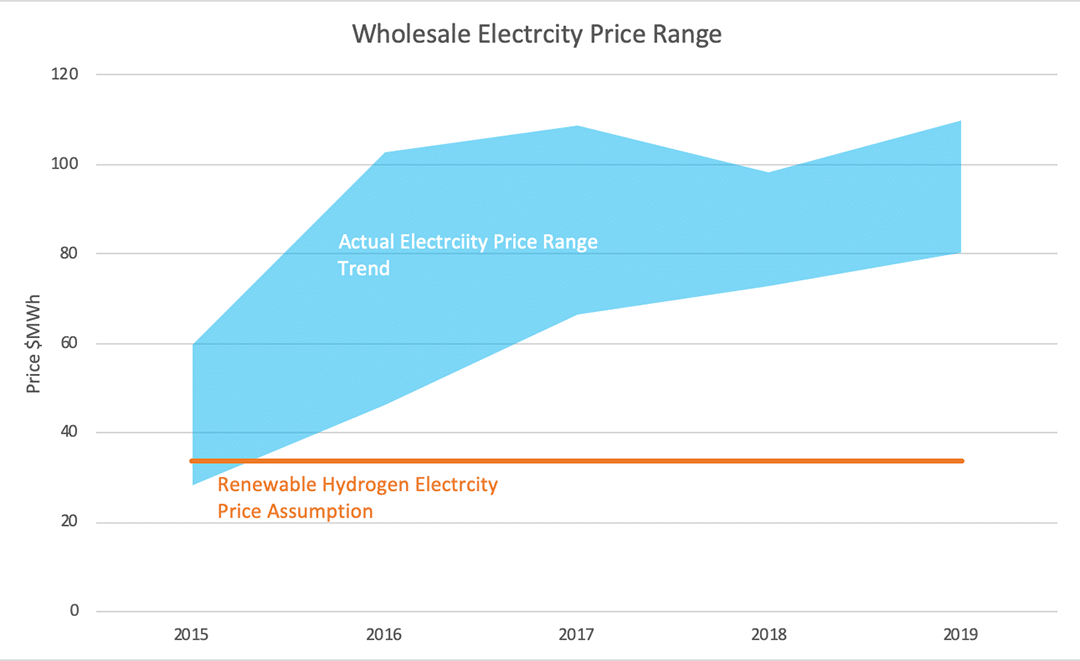

To achieve the A$1.17 reduction from A$3.00, the cost of electricity must decrease by 39%, from A6c to A3.66c/kWh.

As shown in the chart below, wholesale electricity prices were last that low in 2015, before we started closing coal power stations and adding more wind and solar capacity.

What does this mean for the likelihood of the cost of dedicated renewable hydrogen generation dropping from A$11kg (US$7.70kg) to less than A$4.29kg (US$3kg)?

Firstly, the current electricity price of 6c is assumed to be the same for dedicated renewable hydrogen as it is for grid-connected hydrogen (Table 3, above). The main difference is the capacity factor, which is unlikely to change much, given that it is a function of how often the wind blows and the sun shines. We can simply apply the same cost reduction requirement of A$4.21 per kg (US$2.95kg).

Calculation: $11kg - $4.21 = A$6.79 (US$4.75).

Given the data available from the IEA and CSIRO, how did Grattan miss this simple cost barrier?

Even if electricity from wind and solar costs nothing, the projected improvements across the other factors would only bring the cost of renewable hydrogen down to A$4.96kg (US$3.47kg).

Now, some breakthrough in the pipeline may change all that. However, failing to achieve such an unknown breakthrough in the near term will make the cost of dedicated 'green' hydrogen demonstrably too high.

The answer?

CCS hydrogen.

CCS hydrogen is simply hydrogen made from coal or natural gas, with around 95% of carbon dioxide emissions being captured and stored.

The National Hydrogen Roadmap highlights the real export opportunity for Australia to affordably and reliably serve export demand for clean hydrogen by 2030:

Hydrogen production via coal gasification in Victoria’s Latrobe Valley, therefore, represents the most likely thermochemical hydrogen production project.

A prospective plant would have the advantage of an extensive brown coal reserve sitting alongside a well-characterised CO2 storage reservoir in the Gippsland Basin. Pending the success of the proposed HESC demonstration plant in 2020/2021 and subsequent improvements in efficiencies, hydrogen could be produced in the region for approximately $2.14 -2.74/kg under a commercial-scale plant when it comes online in the 2030s.

Source: National Hydrogen Roadmap - Pathways to an economically sustainable hydrogen industry in Australia, page56

And remember, using the Grattan reports own figures, even at this lower price, hydrogen still isn't a cost-competitive way to make steel.

The Opportunity for ECT

Here at ECT, we see two direct opportunities in the context of the emerging hydrogen industry:

- Coldry, our low-temperature lignite drying solution, features zero direct CO2 emissions and can be deployed as the front-end feedstock preparation stage for standard coal gasification technology. This stage is prior to the standard hydrogen production route known as steam reforming. It's the gateway enabler for lignite-to-hydrogen production.

- COHgen, which stands for ‘catalytic organic hydrogen generation,’ is our novel, low-temperature, low-emissions hydrogen generation technology currently under development. It may provide a low-cost alternative to the steam reforming route to produce hydrogen from brown coal.

There is still a lot of work ahead to develop our COHgen process and confirm techno-economic viability at large scale, but we are engaged with various parties involved with the Victorian HESC project, both directly and as a member of the FEnEx CRC – Future Energy Exports Cooperative Research Centre - https://www.fenex.org.au/.

We mentioned above that, even at $2/kg, hydrogen isn’t economically viable for certain applications. Iron and steel making is an example.

We have a solution for that too.

HydroMOR, which stands for ‘hydrogen metal oxide reduction’, is our lignite-based, hydrogen-driven, low-emission primary iron-making process, which enables the utilisation of alternative low-grade and waste resources, improving primary iron production's economic and environmental outcomes. HydroMOR utilises the Coldry process as its front-end drying and material agglomeration stage.

HydroMOR harnesses hydrogen from lignite directly for primary iron-making without needing a separate hydrogen production plant. The hydrogen is generated in situ from the lignite within the reactor, providing outstanding efficiencies and CO2 reductions of ~30% compared to blast furnace production.

As mentioned, the Grattan report states that 'green' steel will be 60% more expensive even if renewable hydrogen manages to come in at US$3kg.

Conversely, adopting HydroMOR is estimated to save more than 30% on capital costs and around 15% on operational costs compared to a blast furnace operation, reducing the cost of the finished product.

Let's conclude by paraphrasing Aaron Patrick's question:

"Should the government pour $500 million of our taxpayer dollars into a proposal that may, if currently unknown breakthroughs that reduce the cost of wind and solar electricity are discovered, eventually make hydrogen that makes steel that costs 60% more?"

You be the judge.