Investor News

Future Energy Exports Cooperative Research Centre

Environmental Clean Technologies Limited (ASX: ECT) (ECT or Company) is pleased to advise the formalisation of its participation in Australia’s leading hydrogen industry development program, the Future Energy Exports Cooperative Research Centre (FEnEx CRC).

Key points:

- FEnEx CRC is helping focus and drive hydrogen research efforts across industry and academia

- Government policy supports a technology-neutral approach, providing clear price and emission targets for industry:

- H2 (hydrogen) under $2 per kilogram by 2030

- CO2 emissions per kilogram of ‘clean’ H2 must be at least 60% less than the ‘benchmark’ threshold emissions of 10.9kg CO2 per kg of hydrogen

- Two hydrogen production pathways will receive support:

- Electrochemical – splitting water using an electrolyser powered by electricity

- Thermochemical – splitting hydrocarbons derived from natural gas, coal or oil, combined with carbon capture and storage (CCS)

- ECT will support the advancement of CCS hydrogen through the development of its two highly prospective technologies:

- COHgen – a unique and novel process for the low-cost production of hydrogen from lignite as an alternative to the gasification-steam reforming process

- Coldry – the world’s only low temperature, low-pressure lignite drying process which also features a net-zero carbon footprint*, providing a cost-effective drying solution for both the COHgen process and the standard gasification-steam reforming hydrogen production process

Further to the shareholder update of 18 June 2020, which briefly mentioned the FEnEx CRC, ECT is pleased to confirm that it has formalised its participation status in Australia’s leading hydrogen research program with the recent signing of the ‘Supporting Participant Agreement’.

ECT Chairman, Glenn Fozard commented, “Hydrogen is emerging as the leading candidate to help decarbonise economies, however the ultimate driver of hydrogen adoption will be price. The secondary driver will be CO2 footprint. Our technologies can potentially help deliver solutions that bring down the cost and CO2 intensity of hydrogen production, enabling Victoria’s vast lignite resource to transition from a source of cheap and reliable, but CO2-intensive electricity generation, to a scalable feedstock for hydrogen production that can support internationally competitive, low-carbon, export-scale production volumes.”

About the FEnEx CRC

The cooperative research centre program, established and administered by the Australian Government Department of Industry, Science, Energy and Resources, supports Australian industries by helping companies’ partner with the research sector to solve industry-identified issues.

The FEnEx CRC aims to execute cutting-edge, industry-led research, education and training to help sustain Australia’s position as a leading LNG exporter, and enable it to become the leading global hydrogen exporter.

There are four research programs:

- Efficient LNG Value Chains

- Hydrogen Export and Value Chains

- Digital Technologies and Interoperability

- Market and Sector Development

ECT will be participating under program 2, Hydrogen Export and Value Chains, which will focus on addressing the following research challenges:

- Processing and delivery methods for cost-effective large-scale hydrogen export

- Target export markets, including key applications and requirements

- Supply chain architecture, design and operations

- Export-class systems and technologies for hydrogen production, storage and delivery

There are two ways the Company will seek to support the thermochemical hydrogen production route, specifically for lignite resources:

- COHgen, which stands for ‘Catalytic Organic Hydrogen generation’, is a novel, low temperature, low emissions hydrogen production technology under development that may provide a lower-cost alternative route to produce hydrogen from brown coal

- Coldry, the gateway enabler for lignite-to-hydrogen production, providing the frontend drying solution to COHgen and supporting project developers electing to use conventional hydrogen production technologies (gasification & steam reforming), coupled with CCS

The FEnEx program will assist ECT to validate the scale up of COHgen in collaboration with industry leaders (energy producers) and end users (energy consumers) and to identify the range of performance indicators and benchmarks for the production of hydrogen from brown coal.

ECT gratefully acknowledge the Department and CRC organisers and looks forward to working closely with the other CRC participants to develop Australia’s hydrogen Industry.

Background to the emerging hydrogen opportunity

Hydrogen itself is not a fuel. Rather, it is a store of energy that can be released via a fuel cell or direct combustion, with the benefit of zero CO2 emissions.

However, while hydrogen is the most abundant chemical element in the universe, unlike oil, coal and natural gas, hydrogen doesn’t occur naturally by itself. It’s either combined with oxygen, to form water (H2O) or combined with carbon, to form hydrocarbons such as those found in natural gas (CH4) and other fossil fuels.

As such, it needs to be produced by one of two paths:

- Electrochemical – splitting water using an electrolyser powered by electricity, featuring high cost and zero direct CO2 emissions

- Thermochemical – splitting hydrocarbons derived from natural gas, coal or oil

At present, ~96% of the worlds annual production of 70 million tonnes of hydrogen is produced via thermochemical methods, utilising natural gas, coal or oil.

Public discourse regarding the best path forward for hydrogen production is a polarising topic for many. Due to concerns over CO2 emissions, debate is often partisan and mired in claims that hydrogen produced via electrolysis using renewable electricity is good and coal or natural gas-derived hydrogen is bad, or vice versa.

Fortunately, Australia’s ‘National Hydrogen Strategy’ and ‘Technology Investment Roadmap’ have adopted a technology-neutral approach focused on supporting the development of a competitive, scalable hydrogen industry, by setting outcome-driven key criteria that seek to balance affordability, reliability and emissions intensity:

- Price - $2 per kilogram by 2030

- Low carbon – CO2 emissions need to be at least 60% below the current ‘best available technology’

These targets allow for the deployment of thermochemical hydrogen production, combined with carbon capture and storage (CCS).

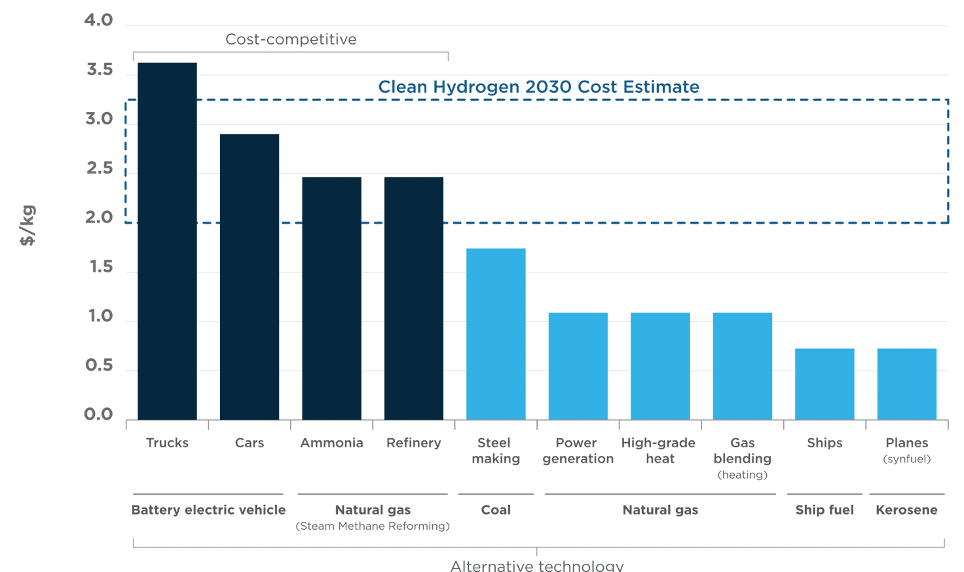

The price of $2/kg is the target for export hydrogen to be competitive with oil and LNG. Domestically, hydrogen may be viable in a range of applications at different price points, as shown in the following table from the National Hydrogen Strategy.

Source: National Hydrogen Strategy, Figure 1.3 - Breakeven cost of hydrogen against alternative technology for major applications, in 2030. Chart is illustrative, as the exact breakeven point will be region-specific, and will be different when comparing to other alternatives (such as petrol or diesel).

The low carbon ‘Guarantee of Origin’ scheme is proposed to be based on the European CertifHy scheme, which has set a benchmark of ~91g per MJ/~10.9kg CO2 per kg H2. This positions the threshold at ~36.4g per MJ or ~4.36kg per kg H2.

Thanks to this technology-neutral approach a Japanese consortium has embarked on a $500 million pilot project, called the Hydrogen Energy Supply Chain (HESC) project, to demonstrate the full supply chain, starting with hydrogen production from brown coal in Victoria’s Latrobe Valley and ending with its transportation to Japan.

Why CCS Hydrogen is the current front runner

To understand why CCS hydrogen is the steppingstone toward a potential renewable hydrogen future, it’s important to identify the significant cost challenges facing renewable hydrogen.

The National Hydrogen Roadmap is clear in its assessment of the cost challenges facing both renewable hydrogen and CCS hydrogen.

In the case of renewable hydrogen electricity input is considered in the context of 3 options:

- Grid connected: Electrolysers draw electricity directly from the network. Despite the emissions intensity of the network, low emissions electricity can still be utilised by securing power purchase agreements (PPAs) with utilities for low carbon electricity.

- Dedicated renewables: Behind the meter (or off grid) electrolyser connection to dedicated renewable energy assets such as solar PV and wind. Electrolysers co-located with both solar photovoltaic (PV) and wind will allow for a higher capacity factor.

- Curtailed renewable energy: Energy is sourced directly from the grid but only when there is surplus renewable energy available (or sourced directly from renewables when the economics do not favour export to the grid).

The three options outlined above represent a trade-off between electricity pricing and capacity factor as presented in terms of the levelised cost of hydrogen (LCOH) in the table below.

| Grid Connected | Dedicated Renewables | Otherwise Curtailed Energy | |

| Average electricity cost (c/kWh) | 6 | 6 | 2 |

| Average capacity factor (%) | 85 | 35 (Co-located PV and wind) | 10 |

| LCOH ($/kg) | ~$6.60 | ~$11 | ~$26 |

The Australian grid has a CO2 footprint of 0.75t/MWh, translating to a CO2 footprint for grid connected hydrogen production of around 40kg CO2 per kilogram of hydrogen.

Based on the proposed target for clean hydrogen of ~4.36kg of CO2 per kilogram of H2, grid connected hydrogen generation would be non-compliant. It will remain non-compliant until grid emissions are reduced by ~90%. There are currently no plans to target this level of CO2 reduction by 2030 by either of the major political parties.

As such, dedicated renewable electricity generation would be required to power electrolysers. Therefore, the challenge is to bring the cost of dedicated renewable hydrogen down from $11/kg to $2/kg. The National Hydrogen Roadmap provides a best case estimate for grid connected renewable hydrogen of $2.29-$2.79/kg by 2030, implying savings of up to $4.64/kg. Applied to dedicated renewable hydrogen, these savings would result in a cost of over $6/kg, well above the $2/kg target. An unknown breakthrough is required to overcome this barrier.

In the case of CCS hydrogen, modelling was undertaken by the CSIRO to assess the competitiveness of brown coal to hydrogen production with reference to clean hydrogen from Victorian lignite. If successful at demonstration, it is expected that the LCOH for a commercial plant will be in the order of $2.14-$2.74/kg, well within striking distance of the $2/kg target and compliant with the clean hydrogen certification criteria.

Based on this data and the supportive policy settings, it is clear that CCS hydrogen is likely to emerge as the leading production route able to meet the cost and CO2 targets in support of an internationally competitive hydrogen export capability.

For further information, contact:

Glenn Fozard – Chairman [email protected]

* Net-zero CO2 emissions: Industrial applications such as power stations and gasifiers generate heat and typically feature substantial waste heat streams. Waste heat is too low in temperature to provide useful work. The Coldry process is designed to be integrated with such host applications, harvesting the waste heat and utilising it to provide the drying energy needed to evaporate the moisture from the coal. Under this default configuration, the Coldry process has a zero direct CO2 footprint.