Investor News

Shareholder Update

Environmental Clean Technologies Limited (ASX: ESI) (ECT or Company) is pleased to provide the following general update, covering the following areas of interest to shareholders:

- India to defy “China Slowdown”

- Coldry as front-end for high grade PCI coal production

- Project Financing update

India to defy the full effect of the ‘China Slowdown’

The company has progressively advanced its India strategy over the past two years and is currently poised to step forward with significant project partners to progress an integrated Coldry demonstration and Matmor pilot plant, subject to formal receipt of Indian federal government clearances.

The ECT Board is comfortable with the company’s focus on India due to a combination of supportive factors, not the least of which are strong forecast growth in energy and iron production, encouraging policy settings around energy and resource security and the reputation for frugal innovation.

Given recent China-driven financial market turmoil, the company’s focus on India appears to be beneficial on yet another level, insulating the company from the brunt of the inevitable fallout.

Investors will notice stock markets have experienced increased sell pressure due to the mounting fear that the Chinese economy is experiencing a hard landing. Financial media commentators have been talking about the risk to Australia’s economy from China’s slowdown due to its exposure to the China market.

ECT’s Chairman, Mr Glenn Fozard commented “India's economic drivers for adopting technology like Coldry and Matmor operate somewhat independently of the global market's influence due to a stronger policy emphasis on domestic self sufficiency. Enabling technologies contributing to that objective, like Coldry & Matmor, find a welcome reception.”

Arvind Sanger, Founder of Geosphere Capital Management, as cited in a recent CNBC article[1], stated that:

“... China slowdown really is not much of an effect for India from an economic standpoint to the extent that India is very small exporter to China and much more of an importer [from] China. So there is not much of a trade hit that India takes from [the] China slowdown. To the extent that that makes commodities cheaper that is a positive, not a negative for India. So, overall it is a non issue for India

India's growth will be fuelled more by domestic policies around building Infrastructure, reducing interest rates and the 'Make in India' program initiated by the Modi Government, with most experts expecting India to exceed GDP growth of 7% by 2017. India is fast becoming the global engine room for growth to replace China.

The extent of the problem faced by most of the world's established coal miners is apparent in the data from Greg Sullivan, the Australian Coal Association's former deputy chief executive. His report, quoted by Reuters Market Analyst Clyde Russell[2] shows that to make an internal rate of return of 15 per cent, most Australian thermal coal miners need prices above $US100 a tonne and coking coal miners require about $US160 a tonne. The problem in achieving this is made clear when you consider that 'China's marginal cost of production for thermal coal is around $US80-$US100 a tonne', according to Ian Roper, analyst with leading Asian investment broking firm, CLSA quoted in the same article. This likely puts a cap on how high coal prices can rise, as Roper points out that the Chinese are opportunistic importers, buying from overseas when the cost is below that of domestic supplies, but pulling back when it's cheaper to buy locally.

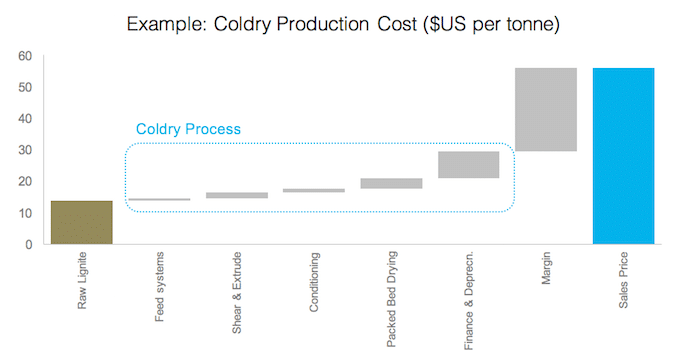

This effect only adds to the opportunity for Coldry adoption given that the anticipated marginal cost to an existing lignite mine of adopting Coldry is expected to be well under the low end of Chinese marginal costs for thermal coal production, reinforcing that Coldry is technically simple and economically powerful. When you add Matmor to the equation, the proposition becomes even more compelling. This is the driver behind the adoption of a Coldry and Matmor integrated plant by our intended Indian partners at Neyveli.

Note: The chart shows an example breakdown of projected incremental costs of a Coldry delivered tonne drawn from an existing lignite mine. Lignite supply is shown as incremental cash, whereas Coldry is fully loaded, allowing an appropriate comparison of Coldry black coal equivalent vs. thermal coal on an incremental basis.

"Global fears of a China slowdown and ailing commodity prices like coal and oil are presenting a significant challenge for the incumbents in the industry. Australian coal miners are operating on the 'breadline' with no immediate relief in sight. Albeit, most experts see this as a China led 'supply shock' that will eventually lead to stronger global growth and strong demand for energy commodities into the future", noted Chairman Glenn Fozard.

"The world doesn't stop producing commodities, rather more attention will be directed to how to produce these commodities at lower cost. This places ECT and our Coldry and Matmor solutions in prime position as the world's industrial heavyweights increasingly turn to technology to improve their margins for the next swing upwards in the commodity cycle."

Building on this view, ECT is pleased to announce the start of a techno-economic feasibility study for the production of high-grade PCI coal in Australia, derived from a Coldry front end drying plant, utilising lignite as the feedstock.

Coldry as front-end for high grade PCI coal production

PCI coal is used in modern blast furnaces to contribute thermal energy and to reduce the total requirements for coking-grade coal. It is a premium product over thermal coal, which cannot be used in blast furnaces.

Recent results from an independent study by a top tier Australian university have highlighted the effectiveness of Coldry pellets as a superior front-end feedstock to produce a high-grade PCI coal product via subsequent further upgrading via pyrolysis. ECT’s Managing Director Ashley Moore stated “PCI has stringent quality and performance criteria, all of which are able to be met as shown in the analysis made to date. In fact, some aspects indicate superior performance versus incumbent materials, which provides market leverage when entering this space. The techno-economic feasibility study will incorporate market analyses, cost of production and capital cost estimations, as well as potential profitability assessment. Our initial evaluation of the potential for this project is very encouraging, and this study is the logical next step.”

Project Finance

In a recent announcement (19 August 2015), ECT advised it was in the process of developing a range of project financing options. Subsequent speculation on the type of funding being considered has resulted in a number of misleading suggestions which the company now clarifies.

All current debt financing packages considered to date are generally non-dilutive and are factored against the project’s expected AusIndustry R&D refund. This requires that the project must receive an Overseas Ruling or Advance Finding from AusIndustry prior to approval, as well as meeting a number of other conditions precedent.

ECT has been a regular recipient of AusIndustry R&D refunds over the years and is currently seeking to satisfy all conditions precedent of the ~A$30 million debt facility prior to formal submission for approval.

The company will provide further updates on this as the considerations progress.

For further information, contact:

Ashley Moore – Managing Director [email protected]

References:

[1] CNBC’s ‘Money Control’ website, 8 July 2015 – www.moneycontrol.com

[2] Sydney Morning Herald 14 Aug 2013