Investor News

Developing 'fit for purpose' Coldry pellets for key markets

Exportability, robustness, durability, and friability are words used to describe coal's general physical handling characteristics.

So, how does the Coldry product hold up under the rigours of transport and handling?

Historically, we've focused our updates largely on the Coldry process and its development, rarely discussing the parallel and ongoing development of the Coldry pellet itself.

And until recently, we'd focused exclusively on developing one type of Coldry pellet: Coldry BCE.

We coined the term BCE, or black coal equivalent, in reference to its higher energy value and ability to substitute for black (thermal) coal in power generation. It was developed to be as robust as possible and, as testing showed, stood up reasonably well to handling compared with regularly traded thermal coal.

The focus on this type of pellet has always been a sensible play into a growth commodity market. Its unique differentiator is that it also leverages lower-value coal assets and mitigates the CO2 intensity of wet, inefficient low-rank coal in power generation.

However, as we’ve engaged with various end users representing a number of applications, we noted some didn’t need the standard pellet we’d been focused on developing. Instead, they were after the lowest-cost path to lignite drying for downstream coal conversion processes, with little call for ‘export’ toughness.

Evolving in response to the opportunities in different markets for different types of dried lignite, we've been working on engineering and tailoring Coldry pellets for specific applications. We believe we've developed a diversified approach that hits the sweet spot in each of those target markets.

Let’s now take a deeper look at Coldry pellet development and its implications, starting with a little background on coal specifications and applications:

As a new product in the global thermal coal market, Coldry will naturally be compared with various coals and pegged to existing benchmarks to understand its physical suitability for consumers' needs and also to arrive at a price.

There are several market indicators for a range of coals. Benchmark specifications around energy, sulphur, ash, and moisture content are identified, and pricing is assessed. Premiums and discounts are applied depending on the coal's differences. Lower ash and sulphur attract a premium. Lower net energy content results in a discount vs. the benchmark.

What isn't always apparent to the layperson are the underlying physical specifications of various coals that determine handling performance, such as hardness, sizing, and the propensity to generate fines. These factors are important to consumers of thermal coal, and there are standard clauses in coal sales agreements that limit the percentage of fines in a shipment and specify other performance properties.

Transport, loading and unloading, stacking, and reclaiming from storage piles. All this handling knocks the coal around and generates a certain amount of fines and dust, leading to product loss, environmental issues, and transport costs.

There are several handy measures for different aspects of physical ‘toughness', including:

- Compressive strength: how much weight it can bear before it crushes

- Abradability: the surface breakage rate from being handled

- Grindability: how much ‘energy' is needed to crush and grind the coal to a certain size

With this in mind, let's now take a look at the Coldry pellet, which has evolved to the point where we can tailor a ‘fit for purpose' dry lignite product to specific market needs.

We know Coldry is drier, higher in energy, and isn't as prone to the same high spontaneous combustion risk as lignite. However, it's not as dense as most black coal.

The key, we've found, is balancing ‘toughness' with the requirements of the supply chain.

Too soft, and you end up with too many fines. Too hard, and the product costs more to pulverise before use.

So, where does Coldry stand on ‘toughness'?

The development of today's Coldry pellets was arrived at through several leaps in pellet quality as the process has been developed and optimised across more than 4000 hours of pilot plant research and development.

Between 2011 and 2014, pellet density and compressive strength increased by ~35% and ~90%, respectively, with a corresponding significant reduction in fines generation.

More recently, on top of these pellet improvements, we've successfully trialled a simple add-on technique that delivers an ‘export' product for consumers. This shape is smoother, the size is uniform, and the pellet is a further ~10% higher density and ~20% stronger, generating less dust and fines than standard Coldry pellets. Still, it's not as hard as some thermal coals, making it less energy-intensive to pulverise before use.

The outcome is we're able to ‘program' and ‘tweak' the Coldry process to produce three distinct variants of Coldry tailored to the following markets:

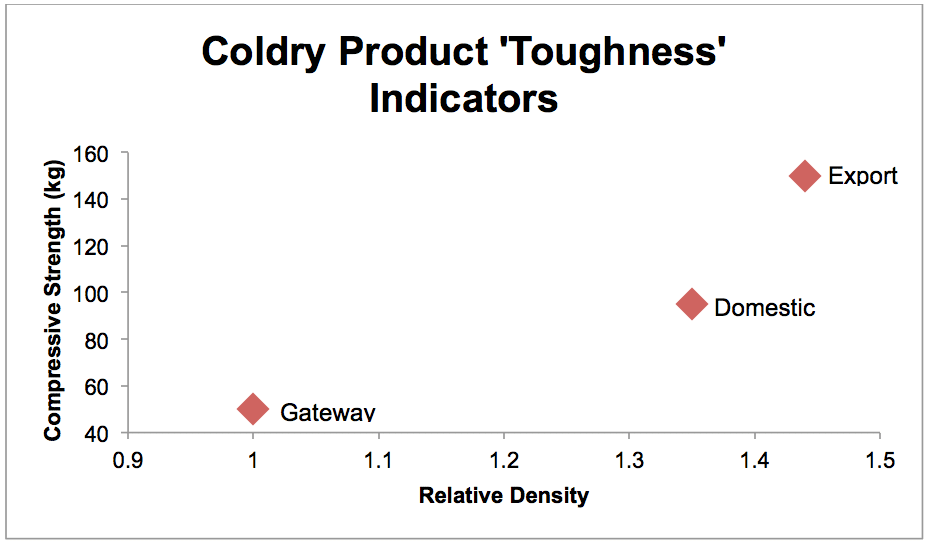

‘Gateway' product: With a lower density, this Coldry product variant can be dried more quickly, lowering production costs. It is ideal for in-situ applications, delivering a dry feedstock into value-added coal conversion processes for pyrolysis, gasification, liquefaction, or power generation.

‘Domestic' product: medium density, suitable for transport and handling environments in local markets. It can be used as a black coal equivalent in thermal coal applications or as a feedstock for more distant value-added coal conversion processes.

‘Export' grade: higher density; this variant is more suitable for markets with harsh transport and handling distribution channels. It can be used as a black coal equivalent in thermal coal applications or as a feedstock for value-added coal conversion processes.

Coldry: Product Diversification

The following chart shows the relative density on the horizontal axis and strength on the vertical axis as an indicator of' toughness'. This illustrates the significant progress in pellet development, driven by the progress and understanding gained through process optimisation studies at our pilot plant.

But what does this mean in practical terms? Developing this fundamental understanding of how changing certain parameters within the Coldry process produces various levels of pellet ‘toughness’, has resulted in the ability to meet the needs of various applications.

Simply put, the ‘Gateway' solution includes significant opportunities for ‘tighter’ integration with downstream processes and can utilise hotter waste heat streams to produce more Coldry from a given plant footprint, lowering the capital intensity and cost per tonne compared to ‘Domestic Coldry. This makes Coldry an attractive front-end drying option for coal conversion processes that are highly sensitive to cost. This is a really compelling scenario, given the expected future requirements for coal-derived products. More on our ‘Gateway' solution in a future article.

The ‘Domestic' product is ideally suited to local supply chains with moderate handling requirements. In terms of deployment, this grade of Coldry can be produced from a Coldry plant bolted onto an existing facility or from a new, tightly integrated plant. The Coldry Design for Tender (DFT) and the current work with Thermax for the proposed demonstration plant in India are geared towards this product type.

The ‘Export' grade Coldry product can also be used locally if desired. It is extremely robust and, therefore, highly suitable for the abrasive and unforgiving handling conditions encountered in supply chains across the seaborne thermal coal trade. The low-cost addition of pellet forming and sizing capability to the existing plant design reaps gains in product durability.

In short, whether the end user is a thermal coal consumer looking for a harder, tougher product or a coal conversion process looking to dry lignite at a lower cost, we've optimised the parameters within the Coldry process to create a product that can meet the application's needs and the end user's price sensitivity.

This, we believe, gives Coldry a much broader application footprint than initially envisaged, creating an even more attractive deployment proposition for lignite resource owners looking to maximise the value of their assets.

For more information on Coldry and its applications, please contact Mr Ashley Moore, Managing Director, at [email protected].