Investor News

Hydrogen explodes

Hydrogen explodes.

The Council of Australian Governments has lifted hydrogen industry development to the top of our national priority list.

There’s a call for feedback and case studies.

It’s all over the news.

This article highlights the key driver for Australia’s efforts: Japan.

This article takes a practical look at how hydrogen can be deployed locally.

Across at internet forum Stockhead, they’ve noticed the hydrogen push, even commenting on ECT’s effort to capitalise on the emerging hydrogen market opportunities.

It seems like everyone is jumping on the hydrogen ‘hype train’.

This is not a recent push here at ECT. We jumped on this hype train a while back, flagging hydrogen as a potential market for our Latrobe Valley Coldry project in 2017 and highlighting the development of HydroMOR and COHgen around the same time.

Our original Matmor process for iron making evolved from a carbon-based process to a hydrogen-based process we call HydroMOR.

Our own hydrogen production process, COHgen, is currently advancing through fundamental R&D with the plan to apply for a patent. If successfully commercialised, COHgen would provide a lower cost, more efficient, and lower CO2 method for hydrogen production from brown coal. Current back-of-the-envelope figures indicate it will be cheaper than dedicated wind and solar-generated hydrogen, even with CCS.

The real battle here will be ideological. 'Green' hydrogen versus 'brown' hydrogen.

Economically, there’s no contest. 'Brown' hydrogen is hands down the cheapest route. Just ask our Chief Scientist, Alan Finkel.

But so far, the news coverage has failed to really explain this, and with good reason. It requires a bit of number crunching, not something the general population digests terribly well.

If you are keen to understand some of the underlying dynamics, we’ve covered hydrogen in several posts:

- Hydrogen fuel scale challenge

- Hydrogen projected to become $2.5 trillion market

- Why should investors care about hydrogen?

- Brown coal the hydrogen economy stepping stone

- Hydrogen the next LNG?

- Hydrogen-fuelled election bid

The bottom line is that meaningful export volumes of 'green' hydrogen would require such a huge addition of wind and solar capacity that the cost would dwarf that of a 'brown' hydrogen facility located in Victoria.

Other factors working against the 'green' hydrogen export model are:

- The dilute nature of wind and solar resources requires vast geographic dispersion, and the associated power network build cost is needed to connect it all back to hydrogen production and storage facilities.

- Then there’s the vast amount of water required. Ideally, seawater would be used, but toxic chlorine gas is formed when electrolysed. Researchers at Stanford may have a solution to this problem, but the problem of scaling wind and solar remains.

- Then factor in the equipment's lifespan. Wind turbines have a ~15-year operational life. Solar panels last about 12 years and have had a decline in performance over that time. A 'brown' hydrogen plant would be erected to last 35-40 years.

- Then there’s the other side of wind and solar that renewables advocates refuse to acknowledge. The emissions that go into the mining, refining and production of wind and solar equipment are not green.

The pros and cons of each are rarely reported in an unbiased manner.

Here’s a quick snapshot to give you a sense of the scale challenge.

Hydrogen Fuel Cell Vehicles

Let’s assume we want to migrate Australia’s passenger car fleet to hydrogen fuel cells supplied by wind or solar.

We’d need ~15,851 wind turbines of 3MW capacity covering ~9,622 square kilometres to produce the ~124.97TWh of electricity needed to 'split' the water.

Australia’s total electricity production in 2016 was ~258TWh, and the total installed wind capacity at the end of 2017 was around ~4,500MW.

To make the switch to HFCVs, we would need to add 10 times more wind capacity, none of which would power our homes.

And solar? We’d need 79,252MW of solar PV capacity. That’s 13 times our 6,000MW of installed capacity (2017).

Putting numbers to the export scale challenge

Let's start with a little background.

Most people understand that wind is intermittent, has low capacity, and has high fluctuations. We only managed to get an average of 30% of our installed wind capacity. Solar also has a low average capacity of 25% but fluctuates less dramatically.

That intermittency means we don’t always have enough electricity flowing from wind and solar at times of demand. This means we need a certain amount of dispatchable power on standby, ready to kick in at a moment’s notice. At present, natural gas-fired power and hydropower are the two main backup sources.

Batteries are touted as a solution, but that’s expensive compared to pumped hydro.

Conversely, there are times when the wind is blowing, and no one needs the electricity. Usually at night.

The idea of ‘green’ hydrogen is to use renewable electricity to split water molecules via electrolysis.

The hydrogen is then stored, and when electricity demand increases and there’s not enough wind output, the energy in the hydrogen is ‘sent’ to the grid via fuel cells.

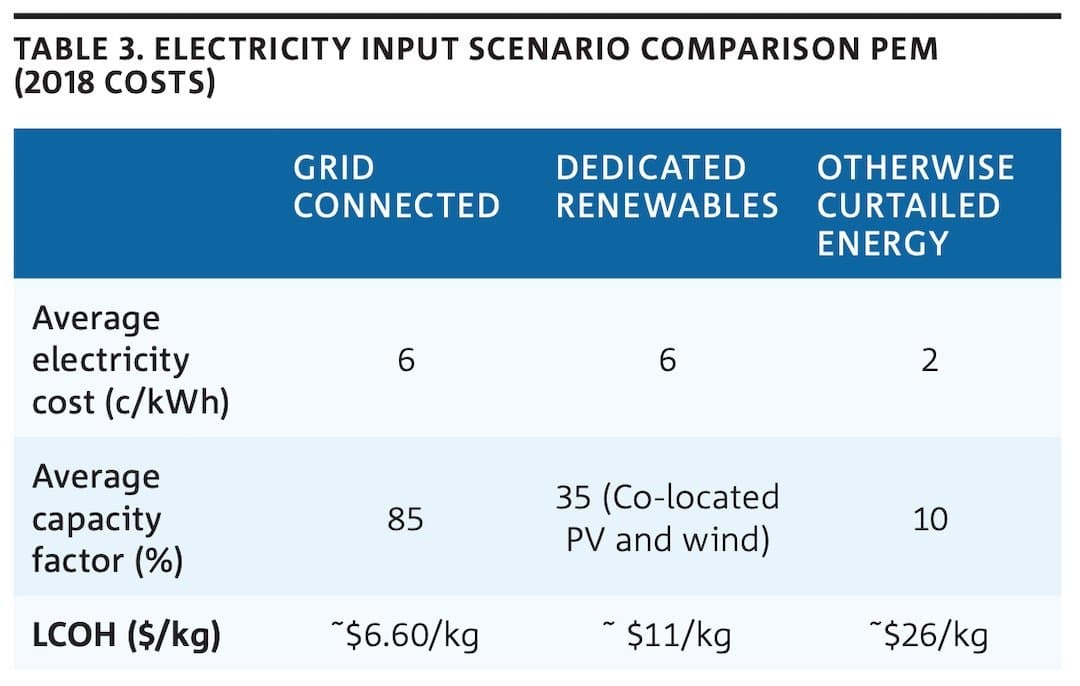

But the CSIRO made the case in its Hydrogen Roadmap report that relying on 'spare' wind or solar costs more to generate hydrogen

National Hydrogen Roadmap. CSIRO, Australia.

At the industrial scale, the CSIRO report suggests a price of around $2.14-$2.74kg for hydrogen produced via brown coal.

The problem with the brown coal route is that it produces CO2, which, in carbon-constrained markets, needs to be either offset or captured and stored (CCS). That adds cost. The above estimate includes the CCS cost and is less than half the cost of electrolysis via grid-supplied electricity, which is almost half the cost of wind and solar-produced hydrogen under 'ideal' conditions.

To be commercial in the transport market, hydrogen must match or beat the price of alternatives: petrol, diesel, and direct charging of battery electric vehicles. Hydrogen needs to enter the market at $8kg to compete with petrol.

Hydrogen must be cheaper than alternatives such as battery storage or pumped hydro to be commercial in the electricity storage market. ARENA outlines particular scenarios for this. They estimate that hydrogen storage for grid firming is cheaper than batteries for 6, 12, and 24-hour storage capacity, while pumped hydro is cheaper than both batteries and hydrogen at all assessed timescales.

The proposed investment in advancing production, storage and distribution solutions is essential if hydrogen is to become cheap enough to replace petrol in the transport sector or provide a cost-effective energy storage solution for our power grid.

This is where COHgen comes in

We’ve been pursuing fundamental research on a potential new hydrogen generation process from brown coal called COHgen, which is catalytic organic hydrogen generation.

Data is still being collected, and hypotheses are being tested, but if we’re successful, COHgen may just provide a cheaper hydrogen generation method than the current gasification-steam reforming route.

In addition to potential cost savings, the CO2 intensity of COHgen is expected to be much lower. How much? We’re still experimenting. But it appears that most of the carbon in our process ends up in solid form as a fine carbon powder. This carbon ‘by-product’ in itself may have potential value in the iron and steel-making markets.

Now for the number crunching.

If renewable advocates demand we abandon ‘brown’ hydrogen, it begs the question: Is there enough ‘spare’ wind (or solar) capacity to supply domestic backup needs and fulfil off-take agreements worth $10 billion a year?

Let’s start by determining how much hydrogen we need to make to export $10 billion worth.

This ACIL Allan report projects the landed price of Australian hydrogen in Japan to be A$4.61kg (2025), or around 2.17 billion kilograms.

How much electricity would it take to make that much hydrogen?

A back-of-envelope calculation:

- It takes around 50kWh of electricity to make 1kg of hydrogen via electrolysis. Advances in efficiency are targeting 43kWh per kg in the next few years.

- Assuming the 43kWh/kg target is achieved, ~93.3TWh of electricity is required to make 2.17 billion kg of hydrogen.

- The NEM generated 260TWh in 2017. Wind accounted for 12.7TWh.

- That 93.3TWh would require ~35,500MW of new wind capacity to be added to the current ~5600MW and any other wind capacity envisaged specifically for electricity generation.

- At 3MW each, we’d need 11,835 wind turbines added to our existing network at a cost of over $25 billion (assuming the cost per MW installed is ~$A2.25 million).

The numbers for taking a solar approach are much worse.

What would a reasonable Hydrogen Industry model look like?

The scale challenge is obvious.

Drill down a level, and it'll be clear to most that the tension between domestic energy demand and exports will create a systemic problem that renewables advocates are desperate to keep out of policy discussions.

Specifically, the more wind and solar are deployed for domestic electricity generation, the more firm backup power is needed. And the more hydrogen directed to firm up unreliable wind and solar, the less we can export.

This is easy to imagine. The domestic-export supply-demand dynamic in the natural gas market has increased domestic gas prices.

And the reliance on ‘spare’ renewable capacity sees the cost of hydrogen skyrocket.

On the other hand, ‘brown’ hydrogen can be scaled to provide dedicated, cost-effective hydrogen production on a reliable, scheduled basis to meet export contracts without threatening domestic backup supplies.

Ideally, if we insist on increasing intermittent forms of energy generation, any ‘spare’ electricity production, which would otherwise be curtailed, should be directed to storage for firming, as intermittency is a direct cost of wind and solar.

Export demand can be met via 'brown' hydrogen without risking export production quotas or domestic supply constraints.

Undoubtedly, this is a complex and fast-evolving area of energy policy discussion. However, it's clear from the outset that those who seek to avoid the topics of scale, cost, domestic electricity production, and domestic firming in the context of achieving exports are hiding something in an attempt to smuggle high-cost 'green' hydrogen into the policy equation without proper scrutiny.

For our part, we look forward to providing feedback to COAG and supporting efforts to leverage Victoria's world-class lignite reserves in pursuit of higher-value, lower-emission hydrogen production.